Millennials Guide For Building A Healthy Credit Profile

The booming retail credit in the country has been propelled by the increasing demand for credit cards, followed by consumer loans. This increase in credit penetration is directly proportional to the rising demand of goods and services by an age-group that comprises two-thirds of the Indian population — the millennials. You may be straight out of college and joining the workforce, or you may already have about 12-13 years of work experience — if you fall into the 20 to 35 years age group, you are a millennial.

In a recent TransUnion CIBIL market survey, the millennials emerged as the fastest growing segment, poised to change the credit landscape with an affinity for credit, financial goals and aspirations.

This group’s credit appetite is fuelled by their aspirations to firstly, upgrade their lifestyles, secondly, purchase vehicles, and thirdly, provide for their families in case of an emergency. If you are a new-to-credit or loan-aspiring millennial, let’s take a look at how you can create a positive credit profile.

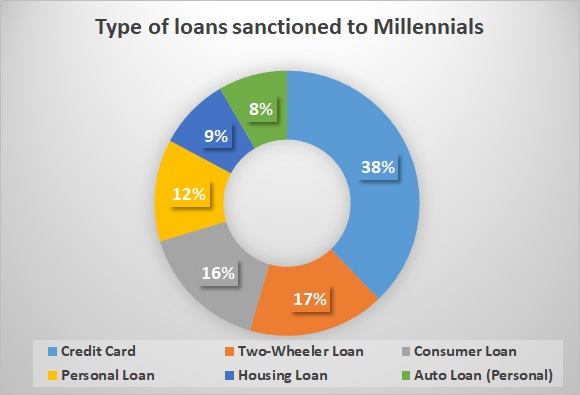

CIBIL data indicates that ~39% of loans were sanctioned to the millennial age group. Within this segment, 38% of loans sanctioned were towards credit cards, followed by two-wheeler loans (17%), and consumer loans (16%).

With most of you in the early stages of your careers, you are exposed to a longer credit lifecycle and may have a larger credit appetite. As per the survey, not only do you agree that loans are the best way to afford an expensive purchase, but are also financially conscious to repay debts on time.

Since access to credit is critical when making a big purchase and/or when there is a medical emergency, there may be a few aspects that new-to-credit millennial should be mindful of.

If you are a millennial, here are key steps that can help you maintain a healthy credit profile:

GETTING STARTED WITH CREDIT

- Create a credit footprint: If you have not used credit before, you will not have a history that lenders can refer to for granting a loan. You can create one by taking a consumer durable loan of a smaller amount (such as a smartphone purchase on EMI) that can be easily repaid.

- Apply for a credit card from the same bank where you have a salary account: A bank that already has your salary account is in a better position to offer you a credit card, primarily because you already have a relationship with them.

- Access credit responsibly: If you are a salaried individual, you may be receiving offers for credit cards with cash-back benefits and higher credit limits. The key is in knowing whether you truly need so many credit cards or not. Do not fall into a debt trap by taking on more cards than you can manage. Instead, start using one credit card responsibly to create a favourable credit history.

BE CREDIT-CONSCIOUS

Make timely payments a habit: Once you do get a credit card, you need to be wary of two key dates—the billing date and, more importantly, the due date. Remember that a single failed payment can affect your credit health and CIBIL score for the next two years. This is because a CIBIL score is based on credit behaviour, and, so, a failed payment today has a long-term effect on your score and your access to credit. A due date reminder on mobile phone will help in timely payment of dues.

While these steps will definitely help you gear up for a positive credit profile, it is imperative to monitor your CIBIL score and report regularly. As you start availing of loan offers, your credit footprint will be recorded and will be a critical factor in determining your access to credit offers later. It is never too early to check your score to ensure correct credit history (or no history), and other information reflecting in your report. Like a reputation, your CIBIL score mirrors your past (credit) behaviour. It will take time and patience to build a good profile, so start working towards a positive credit footprint today.

- Know your credit limits. When availing credit offers, the most important factor to keep in mind is your credit utilisation limits. The optimum range would be to use up to 50% of your card utilisation limit, unless in an emergency. Maxing your cards and failing to pay on time can negatively impact your CIBIL Score.

While these steps will definitely help you gear up for a positive credit profile, it is imperative to check and monitor your CIBIL Score and Report regularly. As you start availing of loan offers, your credit footprint will be recorded and will be a critical factor in determining your access to credit offers later. It is never too early to check your Score to ensure correct credit history (or no history), and other information reflecting in your Report. Like a reputation, your CIBIL Score mirrors your past (credit) behaviour. It will take time and patience to build, so start working towards a positive credit footprint today.

Stay credit-ready by monitoring your CIBIL Score & Report.

Disclaimer: The information posted on this blog (Information) is prepared by TransUnion CIBIL Limited (TU CIBIL). This Information is for generic informational purposes only and is meant for consumer education and awareness about credit scores, credit history and credit reporting. The Information posted on the blog does not constitute credit advice and the user will need to consider the same and take independent informed decisions . No part of this Information may be quoted out of context, distorted ,distributed, published and/ or reproduced in any form and manner whatsoever. Consumers are advised that the Credit Information Reports (CIRs) prepared by TU CIBIL are based on collation of information, substantially, provided by credit institutions who are members with TU CIBIL. TU CIBIL is not responsible and /or liable for errors and/or omissions caused by inaccurate or inadequate information submitted to it by credit institutions. TU CIBIL does not guarantee the adequacy or completeness of the Information and/or its suitability for any specific purpose nor is TU CIBIL responsible for any access or reliance on the Information. TU CIBIL expressly disclaims all such liability. Further, this Information is based on the data available with TU CIBIL at the time of publication and therefore may not be up-to-date.