Monitor your CIBIL Score & Report to be always loan-ready

What’s in your CIBIL Report?

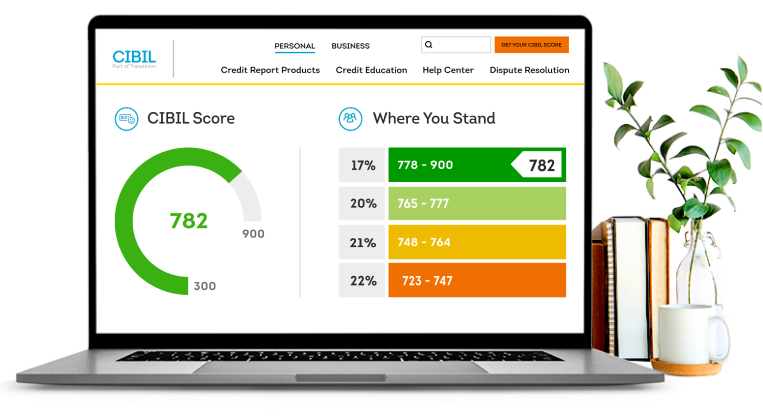

CIBIL Score and Credit Summary

An overview of your credit health, credit worthiness and credit utilization.

Employment section

An overview of your job profile and financials as reported by lenders.

Personal & Contact Information

Includes your name, date of birth, phone numbers, addresses and email IDs.

Account information

Shows all the credit facilities availed, enquiries made and payment history.

Simple & Secure. Get your CIBIL Score and Report in 3 quick steps

1. Create your account with CIBIL

2. Verify your identity

3. Pay & view your CIBIL Score and Report instantly

Checking your CIBIL Score doesn't hurt it

You have questions, we have answers.

Browse our FAQs below.

CIBIL Score is a 3 digit numeric summary of your credit history, derived by using details found in the ‘Accounts’ and ‘Enquiries’ sections on your CIBIL Report and ranges from 300 to 900. The closer your score is to 900, the higher are the chances of your loan application getting approved.

CIBIL Score is required when it comes to loan and credit card applications. Having a high CIBIL score (closer to 900) implies that you have good financial history and lenders express high confidence in extending credit to such individuals. Your borrowing limit and interest can all depend on your CIBIL Score.

Credit Information Bureau of India Limited (CIBIL), which is India’s first Credit Information Company, collects and maintains the records of an individual’s and non-individual’s (commercial entities) credit related transactions such as loans and credit cards. These records are provided by banks and other lenders on a monthly basis to the Credit Bureau. Using this information, a Credit Information Report (CIR) and CIBIL Score is developed.

Your CIBIL score is dependent on various factors. Below are 6 steps which will help you better your score:

- Always pay your dues on time

- Keep your credit balances low

- Apply for new credit in moderation

- Maintain a healthy credit mix of secured (such as home loan, auto loan) and unsecured loans (such as personal loan, credit cards).

- Monitor your co-signed, guaranteed and joint accounts monthly

- Review your credit history frequently throughout the year

When you check your own credit score or credit report, it is counted as a "soft enquiry". Your CIBIL score remains unaffected no matter how many times you check your credit score for yourself. However, if banks or financial institutions check your credit report at the time of new credit card or loan application, it is considered as a "hard enquiry" and impacts your score.

Multiple hard inquiries, if done over a relatively short period of time, demonstrate what is called “credit hungry behaviour” and may hurt your credit score.

We have various plans available based on how long you want access to your report. You can view the plans here. In case you are not interested in any of our paid plans, you can still opt for a Free CIBIL Credit Report here. With free, you will just get a one time score. Other features available in the paid plans such as alerts and score simulator will not be available