Credit Score and Loan Basics

1. What is TransUnion CIBIL? What does it do?

TransUnion CIBIL Limited is India’s first Credit Information Company, also commonly referred as a Credit Bureau. We collect and maintain records of individuals’ and commercial entities’ payments pertaining to loans and credit cards. These records are submitted to us by banks and other lenders on a monthly basis; using this information a CIBIL Score and Report for individuals is developed, which enables lenders to evaluate and approve loan applications.

A Credit Bureau is licensed by the RBI and governed by the Credit Information Companies (Regulation) Act of 2005.

Click here to know more.

2. Why is my CIBIL Score important for getting my loan sanctioned?

The CIBIL Score plays a critical role in the loan application process. After an applicant fills out the application form and hands it over to the lender, the lender first checks the CIBIL Score and Report of the applicant. If the CIBIL Score is low, the lender may not even consider the application further and reject it at that point. If the CIBIL Score is high, the lender will look into the application and consider other details to determine if the applicant is credit-worthy. The CIBIL Score works as a first impression for the lender, the higher the score, the better are your chances of the loan being reviewed and approved. The decision to lend is solely dependent on the lender and CIBIL does not in any manner decide if the loan/credit card should be sanctioned or not.

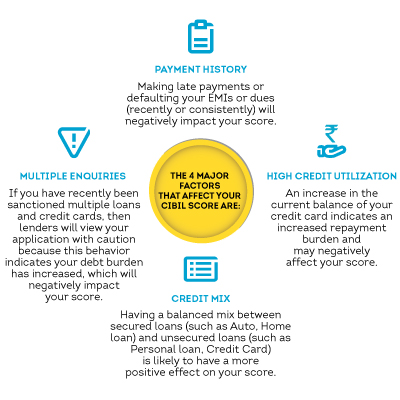

3. What is a CIBIL Score and what factors affect my CIBIL Score?

CIBIL Score is a 3 digit numeric summary of your credit history, derived by using details found in the ‘Accounts’ and ‘Enquiries’ sections on your CIBIL Report and ranges from 300 to 900. The closer your score is to 900, the higher are the chances of your loan application getting approved. It is based on 36 months of your credit history.

Watch this video to know more about the information in your CIBIL Report.

4. How can I improve my CIBIL Score?

You can improve your CIBIL Score by maintaining a good credit history, which is essential for loan approvals by lenders. Follow these 6 steps which will help you better your score:

- Always pay your dues on time: Late payments are viewed negatively by lenders

- Keep your balances low: Always be prudent to not use too much credit, control your utilization.

- Maintain a healthy mix of credit: It is better to have a healthy mix of secured (such as home loan, auto loan) and unsecured loans (such as personal loan, credit cards). Too many unsecured loans may be viewed negatively.

- Apply for new credit in moderation: You don’t want to reflect that you are continuously seeking excessive credit; apply for new credit cautiously.

- Monitor your co-signed, guaranteed and joint accounts monthly: In co-signed, guaranteed or jointly held accounts, you are held equally liable for missed payments. Your joint holder’s (or the guaranteed individual) negligence could affect your ability to access credit when you need it.

- Review your credit history frequently throughout the year: Monitor your CIBIL Score and Report regularly to avoid unpleasant surprises in the form of a rejected loan application.

5. Can CIBIL delete or change my records?

CIBIL cannot delete or change records reflecting on your CIR on its own; we simply collect records of individuals provided to us by our members (Banks and financial institutions). There are no ‘good’ and ‘bad’ credit or defaulters lists either.

6. What does No Hit mean?

A No Hit means that based on the details submitted by you, there isn’t adequate credit activity to generate your CIBIL Score & Report. Please note that the same will be available only when any financial institution submits any information pertaining to your credit activity.